Public companies, private companies, and the insider-trading tripwire

People who tend to fail in public-company life

A private company can feel like a workshop. Tools on the bench. Decisions made close to the work. Conversations stay small.

A public company can feel like a lab with glass walls. People still build things, yet cameras, instruments, and rulebooks sit everywhere. Words travel. Numbers travel. Mistakes travel fastest of all.

Both kinds of company can grow quickly. Both can hire good people and sell good products. The key difference sits in speed.

In public markets, information turns into money in minutes. That single fact reshapes leadership, incentives, and risk.

When a company goes public, it does not only raise capital. It enters an environment where casual speech can become evidence.

What overlaps, what diverges

Where both worlds match

Customers still matter. Cash still matters. Bad decisions still hurt.

Trust still matters. Leaders who earn trust find better terms and better partners.

Takeovers can happen in both worlds, though the paths differ.

The Feel of Private vs Public Companies

Where the worlds split

Private companies run on profit, reserves, and choice.

Owners can grow when growth makes sense. They can slow down to strengthen operations. They can keep strategy quiet.

Public companies run on price, narrative, and compliance.

Share price becomes a scoreboard. Quarterly expectations become a drumbeat. Disclosure rules shape language and timing.

Public markets also reshape the psychology of wealth. Private ownership can feel sticky. Founders often hold tight until they sell the whole business.

Public shares feel liquid. A person can sell part of a position and still stay “in.” The remaining shares can even rise if demand grows. That can feel upside down, and it can pull leaders toward managing the market rather than building the business.

The hidden tax of public life: silence, choreography, and fear

Public-company leadership demands controlled speech.

A friendly sentence can move money. When money moves, regulators and litigators start hunting for cause and effect.

That “tax” often looks like:

blackout windows and trade pre-clearance for insiders

scripted disclosure calendars

investor relations discipline

constant awareness that “helpful” talk can ruin lives

Entrepreneurs often talk big. They exaggerate. They sell the dream. That habit can work in private commerce. In public markets, that habit can cross a line even when no one aims to cheat.

The Tripwire

Three real examples.

Example 1: “Shadow trading” shows how far the rules can reach

Regulators brought a case against Matthew Panuwat using a theory often called “shadow trading.” The allegation described this pattern: he learned material nonpublic information about his employer’s pending acquisition, then bought options in a different public biotech that regulators viewed as a close comparable. A jury later found him liable.

What to learn from it

Insider trading risk can extend beyond “our own stock.” If information about Company A can predictably move Company B, trading Company B can still trigger enforcement.

If the company had stayed private

Private ownership would not protect someone who trades public securities based on inside knowledge learned at a private firm. The trade still happens in public markets. Private status tends to reduce some liquidity temptations, not the rules.

Example 2: The classic breach scenario

Enforcement tied to the Equifax breach illustrates a familiar pattern. Authorities alleged a senior executive traded before the breach disclosure became public. The matter produced charges and later sentencing outcomes.

What to learn from it

A market-moving event plus personal trading creates a clean, time-stamped story. Surveillance systems love clean stories.

If the company had stayed private

No open market would exist for fast selling. That removes the simplest pathway. Yet deception still creates exposure. A private executive who sells private shares, negotiates a buyout, or exits while hiding material facts can still face serious consequences through fraud claims, fiduciary-duty claims, and sometimes securities-law exposure depending on structure.

Private ownership slows monetisation. Private ownership does not clean the behaviour.

Example 3: Tip networks scale because markets scale

The Raj Rajaratnam era showed what happens when inside information turns into a networked product. Enforcement produced major penalties and became a symbol of how far a tip chain can spread.

What to learn from it

Public markets offer two gifts to the wrong person. Liquidity, and scale. A whisper can become millions when a trader can move fast across large positions.

If the companies had stayed private

Monetising tips quickly becomes harder because private shares trade less often and require counterparties and paperwork. Yet the underlying hazard remains. Inside knowledge can still distort private deals, and legal exposure can still arise, even if detection feels less automatic.

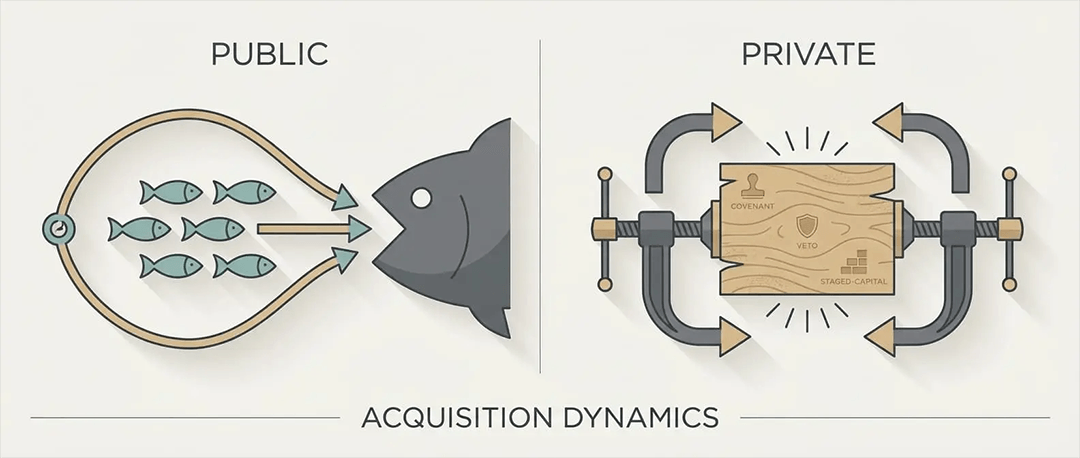

Takeovers: public speed, private leverage

Public takeovers can arrive through the market itself. An acquirer can build a position quietly, then launch a tender offer, an activist campaign, or a hostile approach. A depressed share price can invite predators even when operations look fine.

Private takeovers usually arrive through negotiation. Due diligence goes deeper. A buyer can also take control through softer tools: veto rights, debt covenants, staged investment, or a consortium that slowly cages the founder.

In both worlds, a familiar ending shows up. Builders step aside. Owners step in.

Partnerships: the private-company hazard people underestimate

Private ownership avoids many public disclosure tripwires. It introduces another hazard.

Partnership strain.

Partnerships work when decision rights and exit rules stay clear. They corrode when:

partners want different timelines, or different levels of reinvestment

one partner carries the burden while another carries entitlement

governance stays informal while the company grows complex

resentment grows quietly, then erupts during a crisis or a sale

Public-company life can amplify partnership tension through workload and scrutiny. Private-company life can hide tension until the day everything breaks.

If a private business depends on partnership trust, it needs written structure early. Otherwise, trust becomes the only contract. Trust works. Until it doesn’t.

When Family Life Becomes A Nightmare

Private businesses vs family businesses.

A family business sits inside private ownership, yet it carries its own risk profile.

Common advantages

long-term thinking

loyalty and continuity

patience around investment

Common disadvantages

blurred boundaries between family roles and business roles

reluctant accountability because conflict feels personal

succession problems, especially when heirs want different lives

“employment as love,” where family members get roles they have not earned

difficulty attracting strong outside talent, because outsiders can feel like guests, not leaders

A normal private business can fire someone cleanly. A family business often negotiates with blood ties. That can create stability. That can also create a slow leak of competence.

A Liability In Public Companies

Who should not run a public company

Public-company leadership rewards restraint more than brilliance. Certain temperaments collide with that reality.

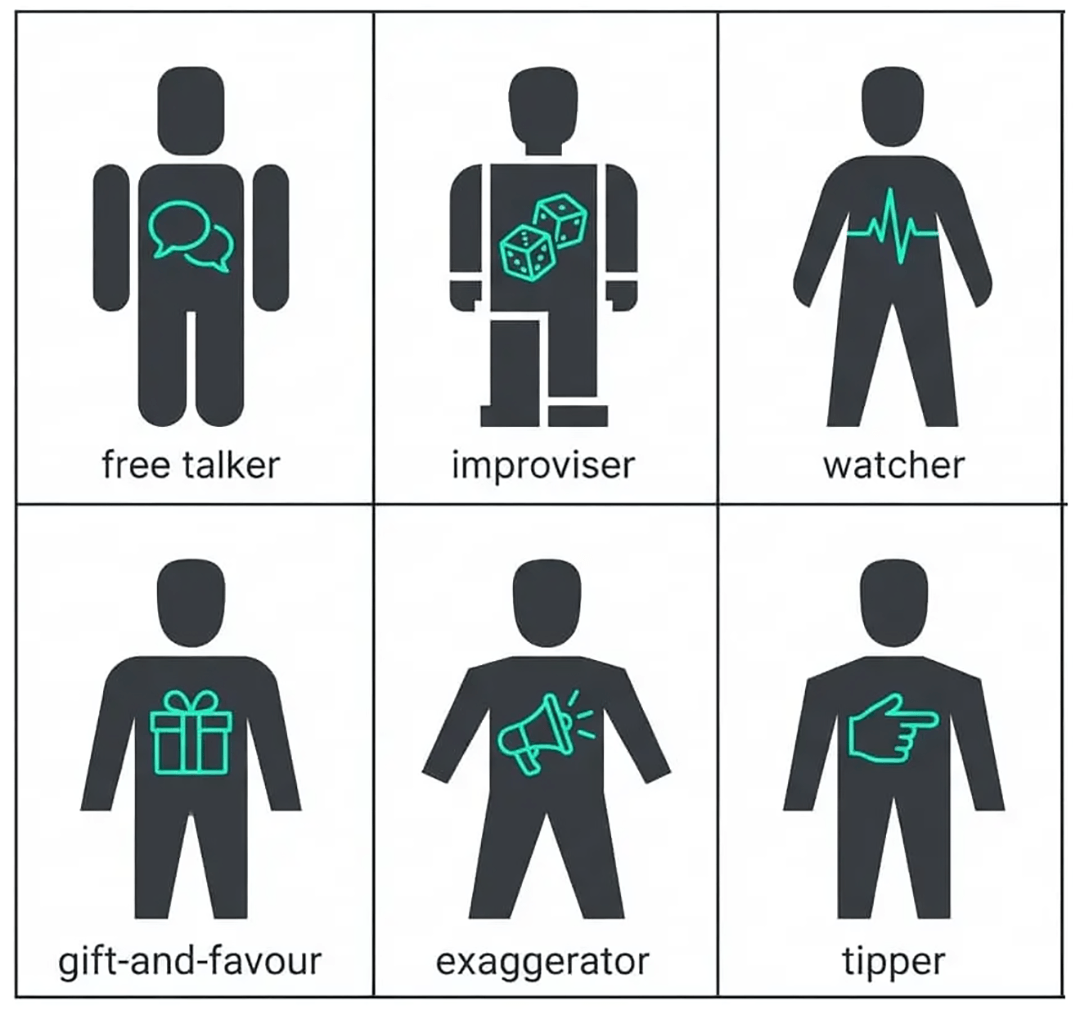

People who tend to fail in public-company life

The free talker. Loves “just between us.” Drops hints. Shares good news early.

The improviser. Treats rules as theatre. Trusts charm more than process.

The tape watcher. Watches the share price like a heart monitor and manages optics over operations.

The gift-and-favour mind. Treats favours and thank-you gifts as harmless. In public markets, gifts can look like benefits tied to inside information.

The entrepreneurial bullshitter. Exaggeration can fuel private sales. In disclosure culture, exaggeration becomes risk.

The helpful tipper. Wants buddies to win. Even inadvertent tipping can create liability and drag colleagues into investigations.

People who usually cope better

detail-driven operators who respect process

leaders who can repeat careful language without boredom

executives who treat compliance as part of performance

Public markets do not punish ambition. Public markets punish looseness. If someone cannot live inside controlled speech and controlled timing, that person can build wealth in private companies, or operate as an investor rather than an insider.

© 2025 Stephen Bray. Patterns in life and business, simply told.